Eli Lilly (LLY) has entered 2026 at a historic inflection point, trading near $920 as it solidifies its position as the leading innovator in obesity, diabetes, and cardiometabolic therapies. With Mounjaro and Zepbound generating explosive revenue growth and new indications expanding the addressable market, Eli Lilly is transitioning from a traditional pharmaceutical leader to the dominant force in the multi-hundred-billion-dollar GLP-1 and weight-loss drug market. Explore the institutional price targets, the pipeline roadmap, and whether LLY stock is a buy in 2026.

In early 2026, Eli Lilly (LLY) has decoupled from traditional pharma cycles. While legacy products provide baseline stability, the GLP-1 franchise (Mounjaro, Zepbound, and emerging orforglipron) has fueled unprecedented revenue acceleration. As of March 2026, the narrative centers on supply chain scaling, new indication approvals, and competitive positioning in the rapidly expanding obesity and diabetes markets. Eli Lilly enters 2026 with massive structural tailwinds. CEO David Ricks continues to emphasize execution on manufacturing capacity and pipeline advancement, projecting sustained triple-digit growth in incretin-based therapies. With record R&D investment and manufacturing expansion, 2026 shapes up as a pivotal year. This guide breaks down the Eli Lilly stock price prediction for 2026 using data from analysts and consensus estimates.

Top 5 Things for Eli Lilly Investors to Know in 2026

- GLP-1 Franchise Dominance: Mounjaro and Zepbound combined revenues exceeded $20 billion annualized run rate by early 2026.

- Pipeline Momentum: Orforglipron (oral GLP-1) and retatrutide (triple agonist) advanced in late-stage trials, expanding future indications.

- Revenue Acceleration: Full-year 2025 revenue reached approximately $48 billion, up 35% YoY, driven by incretin therapies.

- Polarized Targets: Analyst forecasts for 2026 range from bearish lows around $700 to bullish highs of $1,200 to $1,300.

- Valuation Debate: Forward P/E around 50-55x reflects blockbuster growth premium, but pipeline depth and margin leverage support continued re-rating.

What Is Eli Lilly (LLY)?

Eli Lilly is a global pharmaceutical leader specializing in diabetes, obesity, oncology, immunology, and neuroscience. Globally recognized for Mounjaro (tirzepatide), Zepbound, Trulicity, Jardiance, Verzenio, and Taltz, in 2026 it is increasingly classified as the dominant player in the GLP-1 and cardiometabolic revolution. Its core value lies in its incretin-based therapies, deep pipeline, and manufacturing scale. Unlike traditional pharma peers, Eli Lilly's ecosystem includes first-mover advantage in dual/triple agonists, massive supply chain investments, and blockbuster revenue potential in obesity and diabetes.

Eli Lilly's Strategic Evolution (1876-2026): From Pharma Pioneer to GLP-1 Leader

Source: Carson Group

Founded in 1876, Eli Lilly's history features key milestones in drug innovation. Early insulin leadership (1920s) established credibility, followed by Prozac (1980s) and neuroscience dominance. The 2010s-2020s brought oncology and immunology success. The GLP-1 breakthrough with tirzepatide (Mounjaro/Zepbound) ignited the current era. From traditional pharma roots to obesity/diabetes dominance, Eli Lilly has consistently delivered transformative therapies.

Eli Lilly's Key Growth Phases Over the Years: From Insulin to Incretin Revolution

Eli Lilly's journey spans distinct eras:

- Insulin & Neuroscience Phase (1876-2000s): Pioneering insulin and Prozac.

- The Diversification Era (2010s-2020): Oncology, immunology, and diabetes expansion.

- The GLP-1 Dominance Era (2022+): Mounjaro/Zepbound fueling hyper-growth and pipeline acceleration.

Read more: Strategy (MSTR) Stock Outlook 2026: Can MSTR Cross $700 on Bitcoin Treasury Strategy?

Eli Lilly (LLYON) 2025 Performance Overview: The GLP-1 Breakout Year

In 2025, Eli Lilly accelerated dramatically as demand for its GLP-1 therapies, particularly Mounjaro and Zepbound, surged globally across obesity, diabetes, and emerging cardiometabolic indications. While legacy products in oncology, immunology, and neuroscience provided consistent baseline revenue and stability, the incretin franchise delivered explosive, triple-digit growth, transforming Eli Lilly into the clear leader in the rapidly expanding GLP-1 and weight-loss drug market.

Massive investments in manufacturing capacity, supply chain expansion, and late-stage pipeline advancement (orforglipron, retatrutide) fueled momentum, with Zepbound and Mounjaro capturing disproportionate share of the obesity and type 2 diabetes markets. This powerful combination of blockbuster revenue acceleration and long-term pipeline depth drove record financial results, though ongoing supply constraints and high R&D/capital spending introduced temporary margin and cash flow pressure during the aggressive scale-up phase.

1. LLYON Stock Performance, Market Cap Expansion

Eli Lilly's stock exhibited powerful upward momentum throughout 2025, benefiting from broad enthusiasm for GLP-1 therapies, blockbuster revenue visibility, and investor confidence in execution. Shares reached multiple all-time highs during the year, with market capitalization consistently above $850 billion and peaking near $950 billion following strong quarterly earnings beats and positive pipeline updates. The stock traded with elevated volatility relative to traditional pharma names but maintained premium multiples that reflected Eli Lilly's leadership in the multi-hundred-billion-dollar obesity and cardiometabolic markets, while significantly outperforming broader healthcare and market benchmarks in key periods.

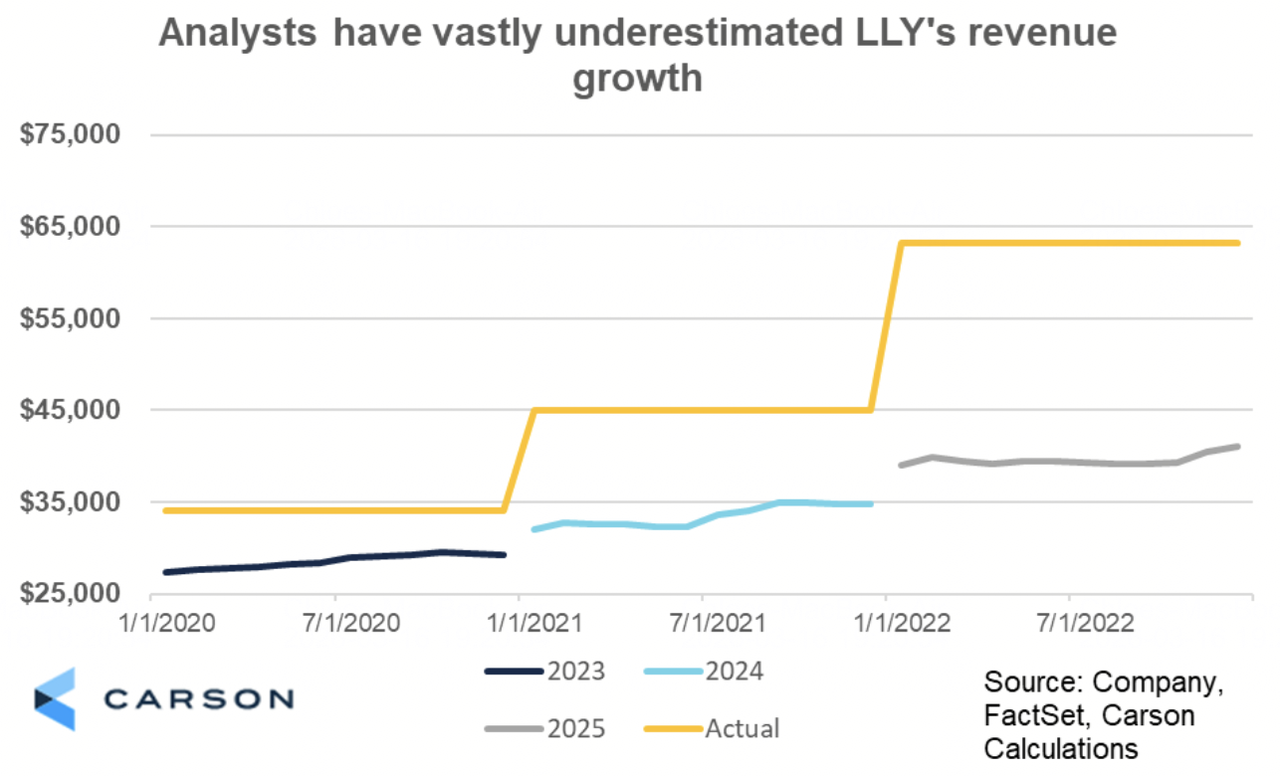

2. Financial Performance: Revenue Hits $48B, Up 35% YoY

Eli Lilly delivered exceptional top-line growth, with full-year revenue reaching approximately $48 billion, up 35% year-over-year. Mounjaro and Zepbound drove the vast majority of incremental revenue, with strong contribution from oncology (Verzenio), immunology (Taltz, Omvoh), and diabetes legacy products (Trulicity, Jardiance). Operating margins improved meaningfully due to scale and mix shift toward high-margin incretins. Net income and diluted EPS rose significantly, supported by robust revenue acceleration despite elevated R&D and manufacturing investments. Quarterly results showed clear momentum, particularly in Q3 and Q4, as supply improvements enabled broader patient access and continued demand growth.

3. GLP-1 Franchise Surge: Growth Exceeds 100%

Mounjaro and Zepbound combined revenues grew at triple-digit rates in multiple quarters, with annualized run rate exceeding $20 billion by late 2025. Demand remained far in excess of supply, even as Eli Lilly significantly expanded manufacturing capacity through new facilities and contract manufacturing partnerships. The incretin franchise captured leading share in both diabetes and obesity markets, driven by superior clinical efficacy, new indications (ex., sleep apnea, heart failure), and growing prescriber and patient acceptance. The performance underscored Eli Lilly's successful positioning as the preferred innovator in the GLP-1 and cardiometabolic space.

4. Strategic Milestones: Pipeline Advancement and Capacity Expansion

Eli Lilly made substantial progress on manufacturing scale-up, bringing new tirzepatide production lines online and securing additional contract manufacturing capacity to address chronic supply constraints. The company advanced orforglipron (oral GLP-1) and retatrutide (triple agonist) in late-stage trials, positioning them as potential next-generation blockbusters with oral convenience and enhanced efficacy profiles. New indications for tirzepatide expanded the addressable market significantly. Eli Lilly also increased its dividend for the 10th consecutive year, reflecting strong cash flow generation and commitment to shareholder returns.

Read more: Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

The Eli Lilly Thesis for 2026: 5 Pillars of LLY Stock Valuation

While legacy products provide baseline stability, Eli Lilly's valuation in 2026 overwhelmingly reflects its leadership in the GLP-1 and cardiometabolic revolution, with Mounjaro/Zepbound revenue, pipeline depth, and manufacturing scale driving the majority of incremental growth and upside potential.

1. GLP-1 Franchise: The Core Growth Layer

Mounjaro and Zepbound (tirzepatide) continue to drive triple-digit revenue growth, with an annualized run rate exceeding $20 billion and expanding indications (sleep apnea, heart failure, NASH) broadening the addressable market to hundreds of millions of patients globally.

2. Pipeline Depth: The Future Layer

Late-stage assets including orforglipron (oral GLP-1), retatrutide (triple agonist), and additional cardiometabolic/oncology candidates provide long-term growth visibility beyond current blockbusters, with potential for multiple next-generation approvals in the coming years.

3. Manufacturing Scale: The Execution Layer

Record investments in internal and contract manufacturing capacity are progressively alleviating supply constraints, enabling broader patient access, higher volumes, and sustained high growth as demand continues to outpace supply.

4. Margin Leverage: The Profitability Layer

Scale benefits from incretin therapies, mix shift toward high-margin GLP-1 products, and ongoing productivity initiatives drive significant operating margin expansion, supporting robust free cash flow generation and premium valuation multiples.

5. Therapeutic Moat: The Defensive Layer

First-mover advantage in dual/triple agonists, superior clinical efficacy data, strong brand leadership in obesity and diabetes, and deep relationships with payers/prescribers create durable barriers, ensuring long-term dominance in the rapidly growing cardiometabolic market.

Eli Lilly Stock Price Forecasts for 2026: LLY's Bull vs. Bear Outlook

Institutional views on Eli Lilly stock remain highly polarized, balancing blockbuster GLP-1 growth against valuation, competition, and supply risks.

|

Institution / Analyst |

2026 Price Target |

Market Outlook |

|

Morgan Stanley (Terence Flynn) |

$1,200 to $1,300 |

Super-Bullish: GLP-1 dominance and pipeline catalysts drive massive upside. |

|

Goldman Sachs |

$1,150 |

Bullish: Maintains Buy on obesity market expansion and manufacturing scale. |

|

Market Consensus (aggregated from MarketBeat, TipRanks, Zacks) |

$1,000 to $1,050 |

Moderate Buy: Balanced view on blockbuster growth and pipeline potential. |

|

JPMorgan |

$950 |

Neutral: Hold rating on execution and competition watch. |

|

Bearish Outlooks (various low-end) |

$700 to $850 |

Pessimistic: Valuation compression, competition risks, supply constraints. |

Source: Aggregated from MarketBeat, Yahoo Finance, and analyst reports as of March 2026

The wide range from bullish targets above $1,200 to bearish calls below $850 captures uncertainty around supply scaling, competition, and valuation sustainability.

The Bull Case: The GLP-1 Surge Drives LLYON Stock Price Above $1,200

Bulls focus on Mounjaro/Zepbound's blockbuster trajectory and pipeline depth. If Eli Lilly sustains triple-digit incretin growth, successfully scales manufacturing capacity, and advances orforglipron/retatrutide through approvals, the company could capture a dominant share of the multi-hundred-billion-dollar obesity and diabetes markets. This positions LLYON as the clear leader in cardiometabolic innovation, supporting targets of $1,200 or higher by year-end 2026.

The Bear Case: The Correction to $850 or Lower

Bears highlight elevated valuation and potential supply/competition risks. If manufacturing constraints persist, competitors gain share, reimbursement challenges emerge, or growth moderates, multiples could compress significantly. Execution or regulatory headwinds would drive the share price lower, with some targets in the $700 to $850 range.

Read more: PepsiCo (PEP) Stock Outlook for 2026: Can PEP Cross $220 on Beverage Portfolio and Emerging Markets?

How to Trade Eli Lilly (LLY) Stock on BingX

BingX offers a versatile ecosystem for gaining exposure to Eli Lilly's 2026 momentum, utilizing BingX AI to provide traders with real-time volatility insights and automated execution strategies.

To buy tokenized stocks like Eli Lilly (LLYON) on BingX Spot:

- Log in to your BingX account and complete identity verification (KYC) if you have not already done so.

- Navigate to the Spot trading section and search for the LLYON/USDT tokenized stock trading pair.

- Choose your order type. A Market Order executes immediately at the current price. A Limit Order lets you set your preferred entry price and waits for the market to reach it.

- Enter the amount you wish to purchase. Because tokenized stocks on BingX support fractional ownership, you can invest with a small amount of USDT rather than having to buy a full share equivalent.

- Confirm the order. Your tokenized stock tokens will appear in your spot wallet once the trade is filled.

Spot tokenized stock trading is best suited for investors who want straightforward buy-and-hold exposure to equity price movements, benefit from 24/7 market access, or are building a diversified digital asset portfolio that includes both crypto and equity-linked instruments.

5 Critical Risks to Watch for Eli Lilly (LLYON) Traders in 2026

While the GLP-1 franchise (Mounjaro, Zepbound) and pipeline momentum offer substantial upside through blockbuster revenue and cardiometabolic market leadership, traders must navigate a complex landscape of regulatory pricing pressure, competitive intensity, supply chain execution risks, reimbursement challenges, and valuation concerns.

1. Regulatory and Drug Pricing Pressure

Eli Lilly faces increasing scrutiny from U.S. and global regulators on high-cost therapies, including potential drug pricing reforms, Medicare negotiation under the Inflation Reduction Act, and international price controls. Adverse rulings, mandatory price concessions, or caps on GLP-1 therapies could materially reduce profitability, limit pricing power, or compress margins on Mounjaro and Zepbound, which drive the majority of recent revenue growth.

2. Intensifying Competition in Obesity and Diabetes

Novo Nordisk (Ozempic, Wegovy) maintains strong brand recognition and market share, while emerging oral GLP-1 competitors, biosimilars, and next-generation therapies from Amgen, Pfizer, Roche, and others are advancing rapidly. If Eli Lilly loses share in the obesity or diabetes markets, Zepbound/Mounjaro growth slows, or competitors gain faster traction with oral formulations or better tolerability profiles, the blockbuster revenue trajectory could moderate, pressuring valuation and growth expectations.

3. Manufacturing and Supply Chain Constraints

Despite massive investments in manufacturing capacity, supply shortages for tirzepatide (active ingredient in Mounjaro/Zepbound) have persisted in 2025 and could continue into 2026. Any delays in scaling production, raw material shortages, quality issues, or regulatory hurdles at new facilities could restrict patient access, limit revenue potential, and frustrate demand, leading to lost market share and investor skepticism about execution.

4. Reimbursement and Payer Dynamics

Widespread insurance coverage and reimbursement for obesity drugs remain inconsistent in many markets. Payer restrictions, step therapy requirements, prior authorization hurdles, or reduced coverage decisions in 2026 could slow patient initiation and adherence, capping real-world demand growth. Any shift in payer policies—especially in the U.S. commercial and government channels—would directly impact volume and revenue ramp for Zepbound and future indications.

5. Patent, Biosimilar, and Long-Term Pipeline Risks

While Eli Lilly enjoys strong patent protection on tirzepatide through the early 2030s, any legal challenges, earlier-than-expected biosimilar entry, or pipeline setbacks (ex., delays or failures in orforglipron, retatrutide, or other late-stage assets) could undermine long-term growth visibility. Execution missteps in clinical trials, regulatory approvals, or new indication expansions would also limit the blockbuster runway and expose the stock to significant valuation compression.

Read more: Circle IPO (2025) Everything You Need to Know About CRCL, Valuation, What It Means for Crypto Market

Conclusion: Should You Invest in Eli Lilly (LLYON) Stock in 2026?

Deciding whether to invest in Eli Lilly in 2026 requires viewing it as a high-conviction play on the obesity and cardiometabolic revolution rather than a traditional pharmaceutical stock. For growth-oriented investors with tolerance for high valuation and supply risk, the Mounjaro/Zepbound franchise's blockbuster trajectory (annualized run rate exceeding $20 billion), pipeline depth (orforglipron, retatrutide), and manufacturing expansion support significant upside if execution delivers. Successful scaling and new indication approvals could drive substantial long-term returns.

For conservative or value-focused investors, the elevated multiples (forward P/E 50-55x), intense competition, ongoing supply constraints, payer/reimbursement uncertainty, and regulatory pricing pressures present substantial risks. The stock's performance now ties to multiple binary outcomes: either GLP-1 dominance and pipeline catalysts continue to justify the premium, or competitive, supply, or regulatory headwinds trigger meaningful compression toward more normalized pharma multiples. Closely monitor quarterly incretin revenue trends, manufacturing capacity updates, pipeline progress, payer coverage decisions, and competitive developments as the clearest indicators of whether Eli Lilly can maintain its leadership in the rapidly growing cardiometabolic market.

Risk Reminder: Trading and investing in equities like LLY involves substantial risk of capital loss. Eli Lilly's high valuation, regulatory and competitive exposure, supply chain dependencies, and reliance on GLP-1 execution make it a high-risk asset. Investors should conduct thorough independent research and consider professional financial advice before allocating capital.

Related Reading

- Circle IPO (2025) Everything You Need to Know About CRCL, Valuation, What It Means for Crypto Market

- Strategy (MSTR) Stock Outlook 2026: Can MSTR Cross $700 on Bitcoin Treasury Strategy?

- Robinhood Stock Forecast 2026: $130 Hyper-Growth or Valuation Correction?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- What Are Coinbase Tokenized Stocks COINX and COINON and How to Buy Them?