When Abbott Laboratories reported Q4 2025 results on January 22, 2026, the company delivered solid fundamentals but disappointed the market. EPS rose 12%, margins expanded by 150 basis points, and it announced its 54th consecutive dividend increase. However, revenue of $11.46 billion missed estimates by about $340 million, weighed down by weakness in nutrition and softer diagnostics volumes. Shares fell roughly 5.5% after hours and declined further after the FDA classified the recall of certain FreeStyle Libre 3 sensors as Class I, citing 860 serious injuries and seven deaths. By mid-March 2026, ABT traded near $109 to $111, about 21% below its 52-week high.

The macro backdrop has added pressure. Healthcare and dividend stocks have lagged amid rising oil prices, tariff escalation, and inflation concerns. Abbott also faces company-specific risks, including the Libre 3 recall, financing a $21 billion acquisition, and continued weakness in its nutrition segment.

At the same time, Abbott’s longer-term outlook remains supported by new growth drivers. The Volt Pulsed Field Ablation system received FDA approval in December 2025 and is entering the U.S. market, while the Exact Sciences acquisition is expected to close in Q2 2026, expanding its diagnostics business. The key question is whether these catalysts can help close the gap between the current price and Wall Street’s $133 to $145 target range. This guide examines that outlook using research from major institutional analysts.

Note: Abbott operates on a calendar fiscal year. Full-year 2025 results were reported on January 22, 2026, and Q1 2026 earnings are expected on April 22, 2026.

Top 5 Things Abbott Investors Should Know in 2026

Abbott’s 2026 story balances a strong medical device pipeline against near-term execution headwinds that have pushed the stock toward multi-year lows. Here are five key themes shaping the investment case.

- Full-Year 2025 Sales Reached $44.3 Billion, With 12 Quarters of Double-Digit Device Growth: Total revenue grew 5.7% reported and 6.7% organically. The medical devices segment delivered its 12th straight quarter of double-digit growth, with FreeStyle Libre sales exceeding $7.5 billion, up 17%.

- Q4 Revenue Missed by $340 Million, Sending Shares Down 5.5%: Q4 revenue of $11.46 billion fell short of estimates near $11.8 billion due to nutrition weakness and softer diagnostics volumes. Adjusted EPS of $1.50 rose 12% and met expectations, but the miss and Libre 3 recall pushed the stock toward its lows.

- 2026 Guidance Projects 10% Adjusted EPS Growth: Abbott expects 6.5–7.5% organic sales growth and adjusted EPS of $5.55–$5.80. Consensus estimates 2026 revenue at about $47.9 billion and EPS near $5.68, with Q1 expected to be softer due to acquisition-related costs.

- Volt PFA and TactiFlex Duo Open a New Electrophysiology Cycle: Volt, approved in December 2025, is entering early U.S. rollout with 84.2% freedom from AFib recurrence at 12 months. TactiFlex Duo has launched in Europe, targeting a $10 billion rhythm management market.

- Analyst Price Targets Range From $113 to $158: Wall Street remains broadly constructive, with most analysts rating the stock Buy or Outperform. The average target sits around $133–$139, reflecting differing views on recall resolution, Volt adoption, and Exact Sciences integration.

What Is Abbott Laboratories (ABT)?

Abbott Laboratories is a diversified global healthcare company headquartered in Abbott Park, Illinois, focused on medical devices, diagnostics, nutrition, and branded generic pharmaceuticals. Founded in 1888 by Wallace Calvin Abbott, the company operates in more than 160 countries with approximately 115,000 employees. Its shares trade on the NYSE under ABT and it is a member of the S&P 500 Dividend Aristocrats, with 54 consecutive years of dividend increases as of 2026.

Abbott operates through four core segments. Medical Devices, including cardiovascular systems, electrophysiology, and the FreeStyle Libre platform, is its primary growth engine. Diagnostics provides lab and point-of-care testing solutions, while Nutritional Products includes brands like Similac and Ensure. Established Pharmaceuticals focuses on branded generics in emerging markets. The pending Exact Sciences acquisition will expand Abbott’s diagnostics footprint, pushing total diagnostics revenue above $12 billion.

Abbott's Strategic Evolution: From Pharma to Multi-Engine MedTech Platform

Abbott’s modern structure was defined by the 2013 spin-off of AbbVie, which allowed the company to focus on devices, diagnostics, and nutrition, businesses with more stable revenue and higher switching costs. The 2017 acquisition of St. Jude Medical strengthened its position in cardiovascular and electrophysiology, forming the foundation of its current device leadership.

With diagnostics normalization complete, Abbott is entering a new phase driven by sustained double-digit device growth, the Volt PFA product cycle, and expansion in diagnostics through Exact Sciences. Management positions 2026 as a transition toward a multi-engine growth model rather than reliance on any single segment.

Abbott's Key Growth Phases: 1888 to 2026

- Pharma Foundation and Early Diversification (1888–2012): Abbott built its early business on pharmaceuticals while expanding into nutrition and medical devices through acquisitions. It became a widely held healthcare stock known for steady dividends and consistent earnings growth.

- Post-AbbVie Spin and St. Jude Build (2013–2022): The AbbVie separation repositioned Abbott as a medical technology and diagnostics company. The $25 billion St. Jude acquisition strengthened its cardiovascular leadership, while FreeStyle Libre expanded globally to more than 60 countries. During this period, Abbott also saw a temporary surge in diagnostics revenue driven by COVID-19 testing demand.

- Device-Led Growth Era (2023–Present): With diagnostics normalized, medical devices are now the core growth driver, delivering 12 consecutive quarters of double-digit growth. Electrophysiology launches, CGM expansion, and the Exact Sciences acquisition define the current phase.

Abbott 2025 Performance Overview: Device Strength, Revenue Miss, and Recall Impact

Abbott closed 2025 with record medical device performance and its 10th consecutive year of adjusted EPS growth, but a Q4 revenue miss and a product safety issue in its core franchise weighed on sentiment.

1. Full-Year Revenue Reached $44.3 Billion, Led by Devices

Total revenue grew 5.7% reported and 6.7% organically. Medical devices drove performance, with FreeStyle Libre revenue exceeding $7.5 billion, up 17%, while electrophysiology and structural heart posted double-digit growth. Q4 marked the 12th straight quarter of double-digit device growth. In contrast, nutrition declined 8.9% in Q4 and diagnostics softened as volumes normalized.

2. Q4 Revenue Missed by $340 Million Despite 12% EPS Growth

Q4 revenue of $11.46 billion fell short of estimates near $11.8 billion, driven by nutrition and diagnostics weakness. Adjusted EPS rose 12% to $1.50 and met expectations, but the top-line miss triggered a 5.5% after-hours decline and continued stock pressure into 2026.

3. Margins Expanded, Supporting Consistent Earnings Growth

Adjusted operating margin rose to 25.8%, up 150 basis points, while gross margin reached 57.1%. Full-year adjusted EPS grew 10% to $5.15, reflecting steady profitability despite cost pressures. Management expects further support from its rhythm management portfolio as new product launches scale.

4. Libre 3 Class I Recall Introduced Execution Risk

The FDA classified certain Libre 3 sensors under a Class I recall, citing 860 injuries and seven deaths linked to inaccurate readings. Around three million units were affected, alongside a warning letter and legal action. Although Abbott has addressed the root cause, the issue continues to weigh on investor confidence.

5. Dividend Growth Reinforced Long-Term Stability

Abbott raised its quarterly dividend to $0.63, marking its 54th consecutive annual increase. The annualized yield of about 2.3% stands above historical averages, which some analysts view as supportive for long-term investors.

The Abbott Investment Thesis for 2026: 4 Pillars of ABT Stock Valuation

The investment case for Abbott in 2026 centers on whether near-term headwinds are masking structurally intact growth engines. Most institutional analysts argue they are, pointing to four key drivers not fully reflected in the current valuation.

1. FreeStyle Libre Remains Early in Global Penetration

Libre serves more than seven million users across 60+ countries, with reimbursement in over 40. 2025 CGM revenue exceeded $7.5 billion, up 17%. New clinical data in March 2026 showed improved HbA1c reduction and longer time in range versus fingerstick monitoring, supporting further reimbursement expansion. The launch of Libre Assist, an AI-driven feature within the app, extends the platform into digital health. Analysts view recall resolution and broader reimbursement as key catalysts.

2. Volt PFA and TactiFlex Duo Drive Electrophysiology Growth

Pulsed field ablation is gaining adoption for atrial fibrillation treatment due to speed and safety advantages. Abbott entered the market with Volt in December 2025, supported by strong clinical outcomes, including 84.2% freedom from recurrence at 12 months. TactiFlex Duo launched in Europe in early 2026. With a $10 billion addressable market, analysts see electrophysiology as a multi-year earnings driver.

3. Exact Sciences Expands Cancer Diagnostics Platform

The $21 billion Exact Sciences acquisition is expected to close in Q2 2026, adding a high-growth cancer diagnostics business with projected revenue above $3 billion. The deal expands Abbott’s diagnostics footprint beyond $12 billion annually and strengthens its presence in oncology and primary care. It is expected to be EPS dilutive near term but accretive by 2028.

4. Dividend Growth and EPS Stability Provide Valuation Support

Abbott has increased its dividend for 54 consecutive years, with payouts up more than 70% since 2020. The current yield near 2.3% is above historical levels, which some analysts view as an attractive entry point. Combined with ~10% expected annual EPS growth, long-term return profiles remain competitive with the broader healthcare sector.

Abbott (ABT) Stock Price Forecasts for 2026: Bull vs. Bear Outlook

Abbott’s setup in early 2026 is unusual. A company with a 54-year dividend growth record and 12 consecutive quarters of double-digit device growth is trading near its lows, about 21% below its $139.06 peak. As of mid-March, ABT trades around $109–$111, while Wall Street targets $133–$139, implying ~20–28% upside. The wide range, from $113 to $158, reflects uncertainty around the Libre recall, Volt adoption, and the Exact Sciences integration.

Institutional Price Targets for Abbott (ABT) Stock in 2026

| Institution | 2026 Price Target | Outlook |

| Barclays (Matt Miksic) | $158 | Buy. Highest target. Sees Volt PFA, Libre expansion, and Exact Sciences as three key re-rating drivers not reflected in current valuation. |

| BTIG | $145 | Buy. Reiterated after Volt FDA approval, citing electrophysiology ramp as an underappreciated earnings driver. |

| UBS | Buy (not disclosed) | Buy. Reiterated after Exact Sciences deal, highlighting diagnostics as a strengthened growth pillar. |

| Citi | $136 | Buy. Lowered from $140, reflecting Libre recall uncertainty and near-term EPS dilution from acquisition financing. |

| Oppenheimer | $132 | Buy. Reduced from $140; cautious on integration costs and nutrition recovery, but constructive on 2027 earnings. |

| Mizuho / Bernstein | $125 | Hold/Neutral. Most cautious. Cites leverage, slower nutrition recovery, and CGM execution risk. |

| Wall Street Consensus | ~$133–$139 | Strong Buy. Majority expects recovery if recall resolves and Exact Sciences closes as planned. |

The Bull Case: Catalyst Alignment Could Drive ABT Toward $145–$158

Bullish analysts see a rare entry point, with near-term execution risks masking three converging catalysts. First, resolution of the Libre 3 recall could restore CGM momentum, supported by Libre Assist and potential reimbursement expansion. Second, Volt PFA adoption in the U.S. builds on early European traction, contributing to electrophysiology growth. Third, the Exact Sciences deal creates a diagnostics platform exceeding $12 billion in revenue with high-teens growth. Targets from Barclays and BTIG assume these drivers support EPS above $5.70 in 2026 and $6.20 in 2027.

The Bear Case: Execution Risks Could Keep ABT Near $100–$115

The bear case focuses on unresolved risks. The Libre recall affected about three million units and led to regulatory scrutiny and litigation. Slower remediation or supply disruption could weaken CGM growth below expectations. At the same time, roughly $20 billion in new debt to fund Exact Sciences raises interest costs and integration risk. More cautious targets around $125 reflect a scenario where nutrition remains weak and growth catalysts take longer to materialize. In this case, ABT may stay rangebound between $100 and $115 until clearer signals emerge from upcoming earnings.

How to Trade Abbott (ABT) Stock on BingX

BingX gives users a way to gain exposure to Abbott's stock price without opening a traditional brokerage account, through Ondo tokenized stocks available on spot markets. Availability varies by region and regulatory requirements.

Buy, Sell, or Hold Ondo's Abbott Tokenized Stock (ABTON) on Spot

Users can trade Ondo's Abbott tokenized stocks on BingX Spot using USDT, enabling fractional exposure and access to ABT price movements within a crypto trading environment. ABTON is an Ondo Finance-issued tokenized representation of Abbott Laboratories stock, settled in USDT and tradeable on-chain.

- Create and secure your BingX account: Register on BingX, complete identity verification (KYC) if required, and enable security features such as two-factor authentication (2FA) to protect your account.

- Deposit USDT or supported assets: Transfer USDT into your BingX wallet. Make sure to select the correct blockchain network and review any minimum deposit requirements or fees.

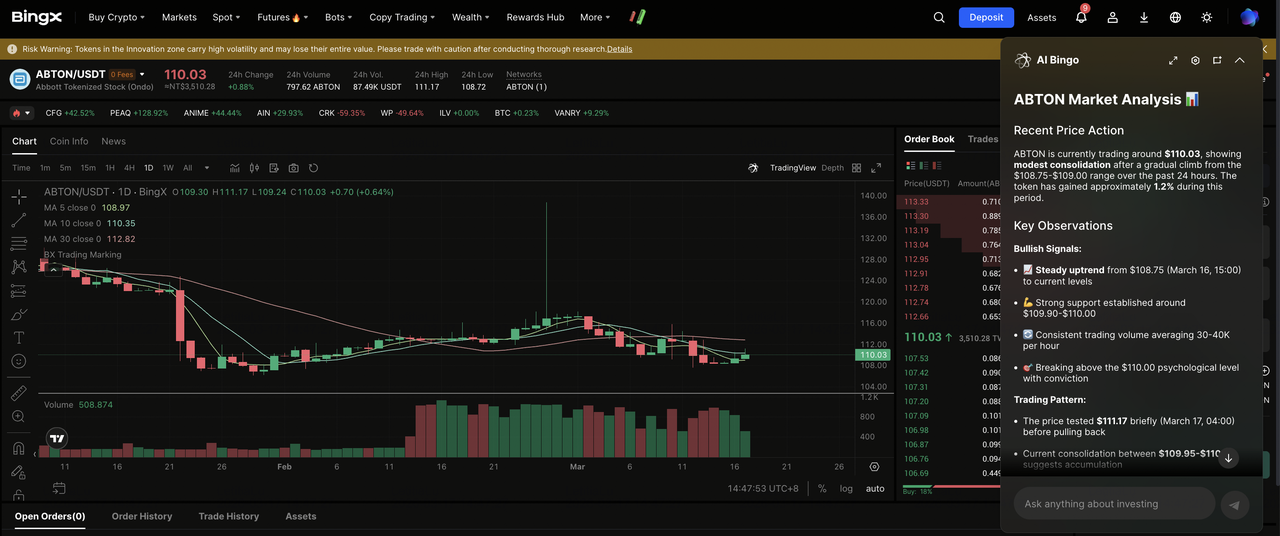

- Search for ABTON in Spot Trading: Go to the Spot market and search for ABTON/USDT. Review the real-time price, order book depth, and recent trading activity before placing an order.

- Use BingX AI to assess market conditions: Before placing an order, you can ask BingX AI about recent ABT price trends, key technical levels, or short-term sentiment related to the Libre 3 recall, Volt PFA launch metrics, or the Exact Sciences acquisition timeline.

- Place your buy order: Choose a market order for immediate execution or a limit order to set your desired entry price. Enter the purchase amount and confirm the trade.

Once completed, your Abbott tokenized stock will appear in your BingX spot wallet and can be held alongside other crypto and tokenized assets.

Top 5 Risks Abbott Investors Should Watch in 2026

Despite Abbott’s strong track record and constructive consensus, several risks have already pressured the stock and could extend the downside.

- FreeStyle Libre 3 Recall and FDA Warning Letter: The Class I recall affecting about three million sensors and the FDA warning letter remain the most immediate risks to Abbott’s core growth franchise. Slower remediation, expanded litigation, or weakened physician confidence could push CGM growth below the 15–17% pace expected by analysts.

- Exact Sciences Integration Complexity: Integrating a $21 billion acquisition while launching new electrophysiology products and stabilizing nutrition creates execution risk. Slower Cologuard growth, higher integration costs, or shifts in the cancer diagnostics market could delay the expected earnings contribution.

- Nutrition Segment Structural Reset: Nutrition faces ongoing pressure from product discontinuation, WIC contract loss, and cost-driven demand softness. Management expects weakness through the first half of 2026, but a longer recovery could weigh on overall growth and put 6.5–7.5% guidance at risk.

- CGM Competition and Pricing Pressure: Competition is intensifying as Dexcom expands its G7 platform and new entrants target the glucose monitoring market. Pricing pressure or share loss in key markets could weaken Libre’s contribution to growth.

- Leverage and Interest Expense Post-Acquisition: The $20 billion debt issued to fund Exact Sciences raises leverage to about 2.7x EBITDA. Higher interest costs could pressure free cash flow and limit flexibility until leverage normalizes.

Conclusion: Should You Invest in Abbott (ABT) Stock in 2026?

The bearish case for Abbott is clear: a revenue miss, a Class I recall in its core franchise, $20 billion in new debt for an acquisition not accretive until 2028, and a nutrition segment without near-term recovery. Together, these explain why ABT has fallen more than 20% from its 52-week high.

Yet the same period also showed continued strength. Abbott delivered its 12th straight quarter of double-digit device growth, 12% EPS expansion, and FDA approval for a new electrophysiology product in a fast-growing category. The Exact Sciences deal positions Abbott in cancer diagnostics, while the FreeStyle Libre platform continues to scale globally with strong clinical support.

With ABT trading near $109–$111, below the $133–$139 consensus range and at an elevated dividend yield, the key question is whether these risks are already priced in. Three near-term signals will matter most: the Q1 2026 earnings update and recall progress, the Exact Sciences integration roadmap, and early Volt adoption in the U.S. If these trend positively, the current valuation may represent an attractive long-term entry point.

Risk Reminder: This article is for informational purposes only and does not constitute investment advice. Abbott stock carries risks including product recalls, integration uncertainty, nutrition weakness, CGM competition, and elevated leverage. Investors should conduct their own research.

Related Reading

- How to Trade Forex, Commodities, Stocks, and Indices With BingX TradFi: A Beginner's Guide (2026)

- PepsiCo (PEP) Stock Outlook for 2026: Can PEP Cross $220 on Beverage Portfolio and Emerging Markets?

- Alibaba (BABA) Stock Forecast for 2026: Can AI and Cloud Growth Push BABA Past $200?

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- McDonald's (MCD) Stock Outlook for 2026: Value King or Margin Trap?