In early 2026, Meta Platforms (META) signaled a shift from 'The Year of Efficiency' to 'The Era of Personal Superintelligence.' Despite legal setbacks in New Mexico and California regarding teen safety, Meta’s core advertising business remains a cash-flow fortress, generating $59.89 billion in Q4 2025 revenue. As of March 2026, the narrative has shifted from the Metaverse to Inference Efficiency, how cheaply and effectively Meta can serve AI to its 3.6 billion daily users.

Meta faces a structural high-stakes year. CEO Mark Zuckerberg has incentivized his top lieutenants with stock options that only vest if Meta hits a $9 trillion market cap, a 580% gain, within five years. While the delay of the Avocado AI model has cooled short-term sentiment, the expansion of the Family of Apps and record-high ad engagement suggest the fundamental floor remains strong.

This guide breaks down the Meta stock price prediction for 2026 using data from Bank of America, Goldman Sachs, and Montaka Global Investments. You will also discover how to gain exposure to Meta Platforms (META) stock futures through BingX TradFi.

Top 5 Things for Meta Investors to Know in 2026

- Efficiency 2.0: Reports suggest a 20% workforce cut of approx. 15,800 jobs to offset massive AI R&D costs and boost operating margins beyond 41%.

- Silicon Independence: The deployment of MTIA (Meta Training and Inference Accelerator) chips aims to save billions in annual infrastructure costs previously paid to Nvidia.

- Ad-Tech Flywheel: AI-powered Advantage+ automation drove a 14% increase in ad impressions and a 6% increase in ad pricing in late 2025.

- Regulatory Iceberg: Meta faces thousands of lawsuits following a $375 million penalty in New Mexico, sparking fears of a Big Tobacco-style regulatory crackdown.

- Polarized Valuation: Analysts targets for META stock in 2026 range from a cautious $496 Bear Case to a bullish $900 from BofA and Investing Group.

What Is Meta Platforms (META)?

Meta Platforms is the world’s leading social infrastructure and AI research company. While its identity is rooted in social networking across Facebook, Instagram, WhatsApp, and Threads, in 2026 it is increasingly viewed as an AI-as-a-Service (AIaaS) and hardware platform. Its value lies in its proprietary social graph and the integration of AI Superintelligence across its hardware like Ray-Ban's Meta glasses and software ecosystem. Unlike cloud providers like Microsoft or Google, Meta’s AI is inward-facing, designed to maximize user engagement and advertiser ROI.

Read more: Top AI Tokenized Stocks to Watch in 2026

Meta's Strategic Evolution (2004–2026): From Social Network to AI Powerhouse

Founded in 2004, Meta’s journey has moved through three distinct eras:

- The Desktop & Mobile Transition (2004–2014): Scaling Facebook and successfully pivoting to mobile ads, followed by the strategic acquisitions of Instagram and WhatsApp.

- The Metaverse Expansion (2021–2023): A controversial rebrand to Meta and billions in Reality Labs spending that initially spooked investors before being paired back.

- The Generative AI & Efficiency Era (2024–2026+): The current phase, where Year of Efficiency cost-cutting meets aggressive Superintelligence spending to dominate the consumer AI assistant market.

Meta (META) 2025 Performance Overview: The Infrastructure Build

In 2025, Meta proved that its AI investments were not just speculative but were actively driving revenue.

- META Stock Reaches $796 High: Driven by stellar earnings beats and AI optimism, Meta shares touched a record high before a late-2025 correction linked to rising capex and legal risks.

- Financial Resilience: Revenue jumped 24% YoY to $59.89 billion in Q4 2025. Operating income hit $24.75 billion, even as expenses swelled 40% due to data center expansion.

- The Avocado Delay: The release of the frontier model Avocado was pushed to May 2026 after internal benchmarks lagged behind Google’s Gemini 3 and OpenAI’s GPT-5.

- Reality Labs Reality Check: While still losing billions, Reality Labs revenue hit $2.2 billion, with Ray-Ban Meta smart glasses emerging as a surprise hit in the wearable AI category.

The Meta Thesis for 2026: 4 Pillars of $META Stock Valuation

- The MTIA Silicon Pivot: By moving inference workloads to its own MTIA chips, Meta can serve AI recommendations to 3.6 billion users at a fraction of the cost of renting external GPUs.

- Monetization Artistry: Meta’s AI doesn't need to be sold like a subscription; it improves the Return on Ad Spend (ROAS). Higher ad performance leads to higher bids from advertisers, creating a permanent revenue flywheel.

- Workforce Productivity: If Meta executes the rumored 20% layoffs, revenue per employee could jump to $3.2 million, far outpacing Microsoft and Alphabet.

- The Personal Superintelligence Vision: Integrating a near-human level AI assistant into Instagram and WhatsApp turns the Family of Apps into the world’s largest AI distribution network.

Meta Platforms (META) 2026 Investment Outlook: The AI Efficiency Pivot vs. Regulatory Headwinds

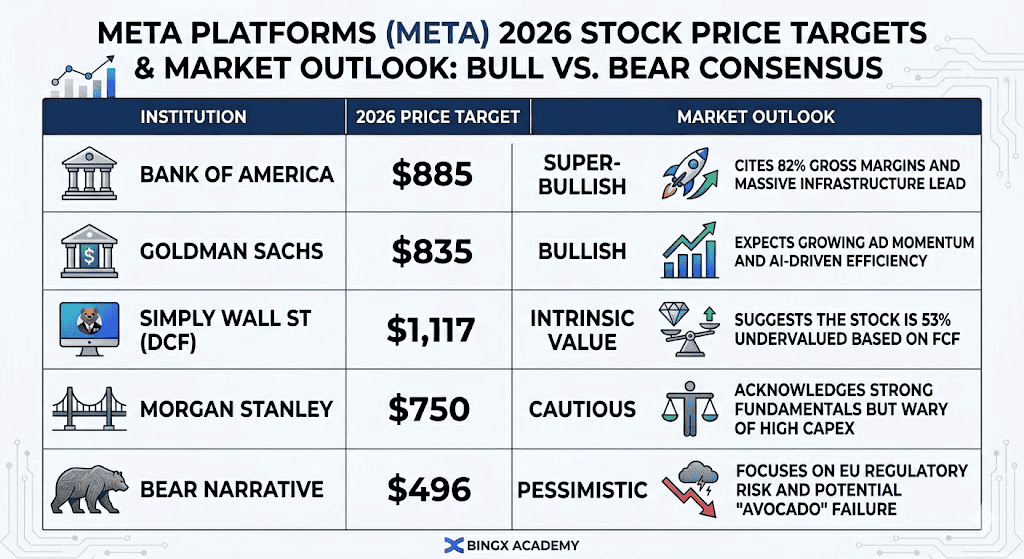

META stock 2026 price targets and mark et outlook | Source: Various analysts

et outlook | Source: Various analysts

The divergence in Meta’s 2026 valuation reflects a high-stakes transition from a social media giant to an efficiency-first AI powerhouse. While technical indicators show the stock trading near a 17x forward P/E, well below its historical mean, the following three scenarios define the price trajectory for the remainder of the year.

Meta Price Forecasts for 2026: Bull vs. Bear Outlook

|

Institution |

2026 Price Target |

Market Outlook |

|

Bank of America |

$885 |

Super-Bullish: Cites 82% gross margins and massive infrastructure lead. |

|

Goldman Sachs |

$835 |

Bullish: Expects growing ad momentum and AI-driven efficiency. |

|

Simply Wall St (DCF) |

$1,117 |

Intrinsic Value: Suggests the stock is 53% undervalued based on FCF. |

|

Morgan Stanley |

$750 |

Cautious: Acknowledges strong fundamentals but wary of high capex. |

|

Bear Narrative |

$496 |

Pessimistic: Focuses on EU regulatory risk and potential "Avocado" failure. |

The Bull Case: The $900 Efficiency Explosion

The bull narrative centers on Meta successfully owning the stack. By migrating massive inference workloads to its MTIA custom silicon, Meta effectively bypasses the Nvidia tax, potentially saving $5 billion to $8 billion in annual OpEx. If the rumored 20% workforce reduction is executed alongside the May rollout of the Avocado AI model, operating margins could surge past 45%. In this scenario, Meta’s AI-powered Advantage+ suite drives a double-digit increase in ad pricing, as advertisers flock to the highest ROI platform in the digital ecosystem.

Institutional bulls like Bank of America and Goldman Sachs eye a target of $835–$900, predicated on Meta achieving a $40+ EPS for FY26. This assumes the Family of Apps maintains its 3.6 billion DAU (daily active user) base while successfully monetizing WhatsApp Business and Ray-Ban Meta smart glasses. For investors, this is a play on Meta becoming the most profitable Physical AI distributor globally, justifying a valuation re-rating toward a 25x multiple.

The Base Case: The $750 Steady Monetization

The base case envisions Meta as a Cash Cow navigating a heavy investment cycle. In this scenario, the $135 billion capex spend is viewed as a necessary defensive moat rather than an immediate top-line accelerator. Revenue continues to grow at a steady 12–15%, supported by Instagram Reels and Threads adoption, but bottom-line growth is tempered by rising depreciation costs from data center buildouts. The Avocado model may not beat GPT-5, but it remains good enough to keep users engaged within Meta’s ecosystem.

Under this outlook, the stock likely settles between $700 and $780, tracking the broader S&P 500's tech recovery. While the Reality Labs segment continues to post quarterly losses of $4 billion+, the core advertising engine generates enough free cash flow to sustain a $50 billion+ share buyback program. This provides a valuation floor, keeping the P/E ratio stable near 19x as the market waits for more tangible Superintelligence revenue.

The Bear Case: The $490 Regulatory Reckoning

The bear case is triggered by a Perfect Storm of legal and product failures. If the March 2026 court losses in New Mexico and California set a precedent for a multi-state Big Tobacco-style settlement, Meta could face tens of billions in liabilities. Simultaneously, if EU regulators under the DMA force Meta to decouple its data-sharing across Facebook and Instagram, the precision of its ad-targeting, and thus its pricing power, would be severely compromised, threatening the 23% of revenue derived from the European market.

In this uninvestable scenario, the stock could retreat to $490 or lower, testing the 52-week support levels. A failure of the Avocado model to launch in May would signal that Meta is losing the AI arms race, potentially forcing a costly licensing deal with Google Gemini. With capex still at record highs and revenue growth stalling to single digits, the 300x P/E on AI expectations would collapse, leading to a massive institutional de-risking of the stock.

How to Trade Meta (META) Stock on BingX

Maximize your trading precision by leveraging BingX AI to analyze Meta’s 2026 volatility patterns and automate your entry strategies across our diverse TradFi instruments.

Buy and Sell Meta Tokenized Stocks METAX and METAON on the Spot Market

METAX/USDT trading pair on the BingX spot market

- Log in to your BingX account and deposit USDT.

- Search for METAX/USDT or METAON/USDT trading pairs in the Spot Market.

- Choose Market or Limit order and enter your investment amount.

- Confirm to hold fractional Meta-linked assets.

Read more: What Is Meta Tokenized Stock (METAX, METAON) and How to Buy It?

Long or Short Meta (META) Stock Futures on BingX TradFi

META/USDT perpetuals on the BingX futures market

- Navigate to BingX TradFi and Stock Futures.

- Select the META/USDT perpetual contract.

- Set your leverage (e.g., 2x–5x) and select Open Long or Open Short.

- Set TP/SL (take-profit/stop-loss) to protect against regulatory-driven volatility.

Read more: How to Trade Forex, Commodities, Stocks, and Indices With BingX TradFi: A Beginner’s Guide (2026)

5 Critical Risks to Watch for Meta Investors in 2026

While Meta’s Superintelligence roadmap offers massive upside, investors must navigate a precarious landscape of regulatory crackdowns, high-stakes capital spending, and intensifying competition in the AI model race.

- The Legal Avalanche: Thousands of lawsuits regarding app addiction could lead to massive settlements or mandatory age-verification changes that slow growth.

- Capex vs. FCF: Spending $135 billion on AI is a big bet. If ad revenue slows due to a macro downturn, the high depreciation could crush net income.

- The Model Gap: If Meta's AI model Avocado continues to underperform, Meta may have to license AI from Google, losing its status as a Frontier Model leader.

- EU Regulatory Heat: The Digital Markets Act (DMA) continues to threaten Meta’s ad-free subscription model in Europe, which accounts for 23% of revenue.

- Execution Risk: Large-scale layoffs (20%) can disrupt internal morale and lead to a talent drain to AI startups like Anthropic or xAI.

Conclusion: Should You Invest in Meta (META) Stock in 2026?

Deciding whether to invest in Meta in 2026 requires balancing its historically low valuation against a backdrop of aggressive capital expenditure and escalating legal scrutiny. At approximately 16x–20x forward earnings, Meta is trading at a significant discount compared to its Magnificent Seven peers, offering a unique entry point for investors who view the current price dip as an overreaction to temporary headwinds. The thesis for 2026 hinges on Meta’s ability to successfully deploy its MTIA custom silicon and finalize its Superintelligence integration; if these internal efficiencies materialize, the company could see a massive expansion in free cash flow, potentially justifying a move toward the $800–$900 price targets set by institutional bulls.

Conversely, for conservative or income-oriented investors, the regulatory iceberg presents a non-trivial threat to long-term stability. The potential for a Big Tobacco-style settlement or restrictive age-verification laws could structurally impair Meta’s primary revenue engine, targeted advertising. Furthermore, the massive $135 billion capex budget places high pressure on the upcoming Avocado AI model to deliver immediate commercial results. A practical strategy for 2026 involves monitoring Q2 operating margins and the progress of pending litigation in California and New Mexico, as these milestones will determine if Meta can maintain its growth at a reasonable price (GARP) status or if it faces a multi-year fundamental correction.

Risk Reminder: Trading and investing in equities like META involves substantial risk of capital loss. Meta’s high volatility, combined with its massive AI infrastructure spending and exposure to evolving global privacy regulations, makes it a high-risk asset. Investors should conduct thorough independent research and consider professional financial advice before allocating capital.

Related Reading

- Microsoft (MSFT) Stock Outlook for 2026: Can Azure AI and Copilot Growth Drive MSFT Stock to $550+?

- Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- Reddit (RDDT) Price Outlook for 2026: Can AI Data Licensing Drive RDDT Back to $200?

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?